Manufacturers are leveraging global insights to address the emerging needs of US laboratories

By Donna Woodall, MT(ASCP)

Donna Woodall, MT(ASCP), Siemens Healthineers.

The clinical laboratory plays a vital role in patient care by delivering to healthcare professionals the diagnostic test results they require to inform critical treatment decisions. However, clinical laboratories are challenged to meet greater testing demands, improve efficiency, and deliver reliable, quality results in the face of labor and budget constraints.

As laboratories focus on reducing cost burdens while meeting increasing testing demands, they are also moving away from buying individual analyzers in the direction of purchasing total solutions that can address both current challenges and long-term needs. Consequently, manufacturers of in vitro diagnostics (IVDs) are leveraging their expertise in global diagnostic trends to bring to market total solutions designed to help meet the needs of the clinical laboratory of the future.

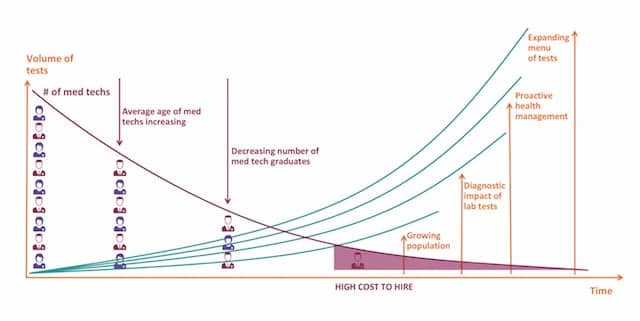

Market trends are forcing adaptation in the clinical laboratory (see Figure 1). The aging population is increasing, and with this rise, the volume of laboratory testing also is increasing. This higher demand on the laboratory, together with test menu expansion, means that today’s labs have to accomplish ever-increasingly more than ever before—but with more stringent budgets. Recognizing that technology can play a critical role in addressing these challenges, manufacturers are introducing comprehensive solutions designed to meet a wide range of laboratories’ needs.

Market Trends Affecting Laboratories

Increased financial pressures and staff shortages are causing labs to rethink their staffing allocations. Relative to the growing volume of tests being performed by laboratories today, there are fewer laboratory technologists processing the ever-growing number of samples. Globally, health worker demand is expected to rise to 80 million by 2030, while the supply of health workers is expected to reach just 65 million over the same period.1 Regions such as Brazil and China are already struggling to adequately staff positions for laboratory specialists and other medical professionals.

Figure 1. The macro trends driving change in the clinical laboratory are focused around how the decreasing population of trained medical and laboratory technicians will keep pace with the ever-increasing testing workload brought on by a growing general population. Combined with an expanding menu of tests and a growing focus on proactive health management, these macro trends are leading manufacturers to create more automated and optimized technology for the central laboratory.

The US Bureau of Labor Statistics reports that between 2012 and 2022 the nation’s demand for clinical laboratory technologists and technicians will grow by 22%. However, the US programs preparing tomorrow’s laboratory workforce are currently training only about half of what is expected to be needed, while approximately 40% of the current laboratory workforce is within 10 years of retirement.2

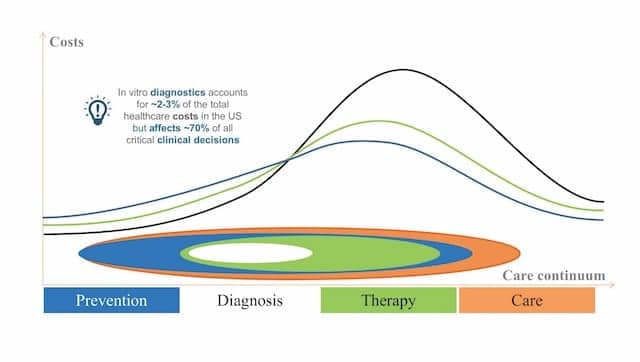

In spite of such challenging market dynamics, the global healthcare community recognizes the importance of clinical laboratory testing for improving patient outcomes. But the extent of that contribution is not widely understood, especially among C-level healthcare executives who are responsible for making major investment decisions on behalf of their institutions and the communities they serve. This is evidenced by the widely accepted estimates that roughly 70% of critical clinical decisions are guided by the results of in vitro diagnostic testing, while clinical laboratories account for only about 2% to 3% of overall healthcare costs.

When patient testing is focused on diagnosis after symptoms have already become manifest—as has traditionally been the case—the impact on the overall continuum of care is that money is funneled into expensive therapies and long-term care. Such delayed diagnosis and intervention ultimately drives up costs while diminishing the quality of patient outcomes (see Figure 2).3

Figure 2. In vitro diagnostics accounts for roughly 2% to 3% of the total healthcare costs in the United States, but affects roughly 70% of all critical clinical decisions. Laboratory diagnostics is relevant to the cost structure of every healthcare system across the entire care continuum.

Value-based healthcare policies are driving the healthcare market toward better patient management by shifting its focus in the direction of prevention and early detection. Examples include Europe’s most economic advantageous tender (MEAT) program, which is a public procurement directive using a life-cycle costing approach to arrive at the best price:quality ratio—essentially the best value for money—for purchased goods and services.4 And in the United States, there has been a similar rise in the development of bundled payment programs intended to standardize care, eliminate unnecessary variation, and improve quality. In the context of such comprehensive care and bundled payment models, early testing with the right technologies can improve patient outcomes through prevention, earlier diagnosis, and focused therapies—ultimately improving overall patient care at a lower total cost.

Reducing Costs and Maximizing ROI

With the aging of populations resulting in increased clinical laboratory testing, both public and private health systems throughout the world are feeling a corresponding need to reduce costs related to patient testing.

In the United States, laboratories are closely monitoring and preparing for implementation of the Protecting Access to Medicare Act of 2014 (PAMA), which will go into full effect in January 2018. PAMA represents the first significant overhaul of the Centers for Medicare & Medicaid Services (CMS) clinical laboratory fee schedule in more than 30 years, and is intended to create a rate-setting system based on average market prices charged for testing services.

Figure 3 The Atellica Solution comprises sample management, immunoassay, and chemistry analyzer components. It delivers unprecedented flexibility to adapt to growing testing needs and space constraints. The Atellica Solution can combine up to 10 components into more than 300 customizable configurations—including linear, L- and U-shapes. It can also connect to Aptio automation to provide a comprehensive multidisciplinary solution or operate as a standalone system.

In effect, PAMA will create a new baseline for the clinical laboratory fee schedule, which serves as the basis for laboratory reimbursement for the government’s Medicare and Medicaid programs as well as for private insurers. When PAMA is implemented, it is expected that reimbursement for many commodity tests could be reduced by as much as 30%. CMS aims to save $3.93 billion in lab reimbursement over a period of 10 years. Private insurers are expected to follow suit and further decrease their reimbursement rates.5

To address these trends, laboratories are moving aggressively toward consolidation, with the expectation that this will enable them to take advantage of economies of scale. Larger hospitals and health systems are pursuing strategic mergers and acquisitions in order to gain market share, achieve cost efficiencies, and wield greater negotiating power over suppliers. Such health systems are also acquiring more pre- and post-acute care facilities and services, as well as physician medical groups, allowing for an expansion of the hospitals’ regional footprint and increased patient engagement through skilled nursing, home healthcare, and rehabilitation services. Meanwhile, small standalone hospitals remain affected by financial pressures, and are gradually dwindling in number as they find that they cannot compete with the large hospital and laboratory networks.

Leveraging Global Best Practices

The fastest-growing and most critical areas of clinical diagnostics are cancer diagnostics, infectious disease tests, and molecular assays and systems. Together, these three areas represent approximately 40% of the IVD market. In the future, they are expected to outpace the growth rate of the overall IVD market.

Globally, specialty testing for the management of critical diseases such as cancer, cardiovascular disease, infectious diseases, and kidney disease accounts for approximately 38% of clinical laboratory revenue. While routine testing boasts a much higher volume of activity, specialty testing is expected to experience double the growth of routine testing over similar periods. The largest areas of specialty testing are esoteric and genetic testing, followed by pathology testing. As the volume of specialty testing increases, laboratories will need to acquire the capital equipment, menu, and experienced personnel needed to conduct such testing.6

Figure 4. The Atellica Solution simplifies laboratory operations through intelligent sample handling. It can process more than 30 different sample container types, including pediatric and tube-top sample cups that can be aspirated from the primary tube. By using the same reagents and consumables across different analyzer configurations, laboratories can streamline inventory and deliver consistent patient results no matter where patients are tested.

To meet their equipment needs for this changing marketplace, labs are transitioning from buying individual analyzers to purchasing total solutions from a single trusted partner. Total solutions encompass a variety of offerings, including equipment for sample management, a broad menu of assays, IVD analyzers, automation systems, and informatics. Taken together, such total solutions are designed to anticipate and address the emerging needs of clinical laboratories.

The shape of such total solutions often originates with the pooled experience and information about diagnostic market trends that IVD manufacturers gather from the global markets in which they operate. Closely observing laboratory trends and collecting information about customer pain points enables manufacturers to respond through continuous investment in technology and innovation. The result is a wide range of options available to laboratories. (For more information, see “Proven Practices for Optimizing a Laboratory with Automation.”)

US laboratorians seeking to adopt a total solutions approach can learn a great deal from their early adopter counterparts globally. In Europe, for example, automated laboratories have become more multidisciplinary, often incorporating hematology, hemostasis, proteins, and urinalysis. And as automated systems become more open—not bound by the limits of proprietary interoperability—other specialty disciplines, such as molecular diagnostics, are also being automated.

Such laboratories capitalize on the benefits delivered by customized automation solutions, such as vertical transport modules that allow samples to travel between different floors, and open systems connecting third-party analyzers to provide integrated and efficient operations. All of these options are brought together through the application of comprehensive information technologies that integrate the entire solution.

Powerful analytical solutions that are fast, flexible, reliable and automation-ready will be key to meeting increasing testing demands and expediting patient results. Siemens Healthineers, Tarrytown, NY, recently unveiled the Atellica Solution, next-generation immunoassay and clinical chemistry analyzers (see Figure 3).7 The Atellica Solution is highly flexible, with more than 300 customizable configurations, and can be connected to Aptio automation for a comprehensive multidisciplinary solution.

Figure 5. One key feature of the Atellica Solution is the Atellica Magline transport, a patented bidirectional, magnetic transport technology that is 10x faster than conventional sample conveyors. It connects the different analytical components and independently transports samples within their analytical testing environment. The transport technology, together with a multicamera vision system, intelligent sample routing, and automatic quality control (QC) and calibration capabilities, give laboratories independent control over every sample—from routine to stat—to speed patient results to clinicians.

The innovative design features of the Atellica Solution include its high level of automation; a sophisticated vision system; automated QC and calibration; and efficient, intelligent sample management and test scheduling (see Figure 4). These features, along with a unique bidirectional magnetic sample transport technology, were purposefully engineered to better utilize the diminishing labor available and to reduce the need for multiple highly skilled operators (see Figure 5).

With increasing test volume and consolidation, analyzers are expected to produce higher throughput and be able to connect to automation tracks in high volume ‘hub’ laboratories, while also providing efficiency and standardization across the laboratory network, including the ‘spokes.’ Prompt turnaround time for test results has high value to physicians, as results may lead to diagnostic decisionmaking that can reduce treatment costs, reduce the length of hospital stays, and improve patient care—all while reducing overall costs.

The Atellica Solution was developed based on an understanding of a number of market trends that are driving the emerging needs of clinical laboratories on a global scale. Mainly, the Atellica Solution is a contribution to helping laboratorians focus on driving better business and clinical outcomes, and spending less time managing their operations.

Conclusion

The clinical laboratory plays a vital role by delivering to healthcare professionals diagnostic test results that are used to inform critical treatment decisions. However, clinical laboratories are often challenged to meet greater testing demands while also improving efficiency and delivering reliable, quality results—even in the face of labor and budget constraints.

As laboratories focus on reducing cost burdens while meeting increasing testing demands such as specialty diagnostic testing, they are moving away from buying individual analyzers to purchasing total solutions that can address both current challenges and long-term laboratory needs. Laboratory diagnostics manufacturers are leveraging their expertise in global diagnostic trends to produce total laboratory solutions designed to help meet the emerging needs of the clinical laboratory of the future.

Donna Woodall, MT(ASCP), is senior director of global marketing for next-generation products at Siemens Healthineers, Tarrytown, NY. For further information contact CLP chief editor Steve Halasey via [email protected].

References

- Liu JX, Goryakin Y, Maeda A, Bruckner T, Scheffler R. Global health workforce labor market projections for 2030. Hum Resour Health. 2017;15(1):11; doi: 10.1186/s12960-017-0187-2.

- Lingo A. US demand for medical technologists reaches boiling point [online]. Cincinnati, Ohio: PassportUSA by Health Carousel, 2016. Available at: https://passportusa.com/med-tech-jobs-in-usa. Accessed June 13, 2017.

- Wolcott J, Schwartz A, Goodman C. Laboratory Medicine: A National Status Report. Columbus, Ohio: Battelle Memorial Institute, 2008. Available at: https://wwwn.cdc.gov/futurelabmedicine/pdfs/2007%20status%20report%20laboratory_medicine_-_a_national_status_report_from_the_lewin_group_updated_2008-9.pdf. Accessed June 13, 2017.

- Most economically advantageous tender (MEAT) [online]. Salford, UK: Crescent Purchasing Consortium, 2015. Available at: http://www.felp.ac.uk/content/most-economically-advantageous-tender-meat. Accessed June 13, 2017.

- Burns J. CMS issues PAMA final rule that aims to cut Medicare’s clinical laboratory test price schedule sharply beginning in 2018 [online]. Dark Daily. July 18, 2016. Available at: www.darkdaily.com/cms-issues-pama-final-rule-that-aims-to-cut-medicares-clinical-laboratory-test-price-schedule-sharply-beginning-in-2018. Accessed June 19, 2017.

- Clinical Laboratory Services Market: Forecasts to 2020. Rockville, Md: Kalorama Information, 2015. Available at: www.kaloramainformation.com/clinical-laboratory-services-9305161. Accessed June 13, 2017.

- Siemens Healthineers unveils game-changing Atellica Solution at AACC 2016 [press release]. Erlangen, Germany: Siemens Healthineers, 2016. Available at: www.siemens.com/press/en/pressrelease/?press=/en/pressrelease/2016/healthcare/pr2016080357hcen.htm&content[]=HC. Accessed June 13, 2017.

{kind=link}